It’s valid to ask: Should I stop regular investments – or mutual fund SIPS, protect my capital and restart once the fall is complete and the market trend turns positive?

This alliteration is likely to cause a lot of anxiety to many investors who are investing regularly in equity markets to create long term wealth. Not only is this long-term wealth eroding fast, but also given the uncertain global environment, one is inclined to believe that there will be more pain.

It’s valid to ask: Should I stop regular investments – or mutual fund SIPS, protect my capital and restart once the fall is complete and the market trend turns positive?

Let’s take this in two parts: Should you stop regular SIPs in equity? Do you need to protect capital?

What happens if you stop SIPs?

The market correction has been rather sharp with a 22% correction In Nifty 50 since the start of the month till 20th March, followed by a 13% fall in a single day on the 23rd of March. While this has resulted in a quick erosion in the value of whatever gains you had accumulated till now in equity, it has also thrown up the opportunity to invest from this point onwards at lower levels.

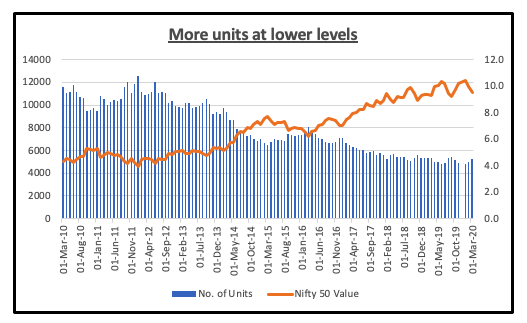

Let’s say you invest Rs 50,000 every month in the Nifty 50 from March 2010, you would have accumulated 827 units of the Nifty 50 till March 2020. Out of these, 63% or 518 units were accumulated till March 2015 which is the mid-way mark (see graph). This happened because markets rose at a faster pace post that and hence, a lower number of units are added each month.

It’s the higher number of units accumulated in the first five years which will add more to your investment value at the end of ten years. At a Nifty 50 level of 11,000, you got 4.5 units invested for a Rs 50,000 investment; now at Nifty 50 level of 8700, your SIP will get you 5.7 units. If you keep adding more units at a lower level, you will gain more when markets return to higher levels. The fall in value enables you to add more units for the same amount of investment. In this way, you have more to gain when the recovery begins as you have added units at a faster pace.

What you need to understand is that the job of your equity investments or your allocation to equity is not to preserve capital. Capital preservation is the job of your allocation to fixed-income securities.

Do you need to protect capital?

When you see the value of your investment falling sharply every day, it's natural to think that you should protect capital and not invest more. However, that means going back on wealth creation. Equity market movement is not linear, which means returns are not spread out equally across the years.

You have to keep investing when the markets correct so that you balance out the investments made when the markets were moving up. If you only invest in an uptrend, your successive monthly investments will add lesser units each month as markets rise (see graph). Investing in corrections is a way to make your capital more efficient as you are able to enhance returns when markets recover.

What you need to understand is that the job of your equity investments or your allocation to equity is not to preserve capital. Capital preservation is the job of your allocation to fixed-income securities.

Capital preservation will seem important now, but you must understand that equity returns help you grow capital in the long run. If you have only one portfolio goal i.e., capital preservation then you needn’t invest in equity. Your equity goal needs to be long term.

Today your long-term equity returns may also look negative, but this will change when the market begins its upward trend. These losses are interim and not actual until you redeem. Stay invested with your existing capital and it’s imperative to continue your SIPs for the most efficient long term returns and wealth creation that equity markets can offer.

Comments

Post a Comment