Armed forces personnel? Know what is commutation & how should you invest your commutation lumpsum.

on

Get link

Facebook

X

Pinterest

Email

Other Apps

Armed forces personnel? Know what is commutation & how should you invest your commutation lumpsum.

Learn how is commutation calculated and how you can go about investing this significant lump sum amount effectively

Commuting your pension is a decision that you will have to make when you are generally a year or less from retiring from the armed forces. The question that quite a few retiring personnel have, is how does it help and how should they invest this money.

How should you make this important decision of investing this money? Let’s explore this question and provide you with a framework to arrive at the right answer for you.

What is commutation?

Commutation is a choice the government gives you between two things. One choice is whether you want to receive your usual pension which is a function of your basic salary pre-retirement.

The other choice is to receive a bulk amount upfront at the cost of a somewhat reduced pension amount – this in essence is commutation.

Now how is this commutation amount arrived at? To answer this question you will first have to understand what makes up your pension.

What makes up your pension?

Your pension is generally half of your last drawn basic salary. This includes basic, grade pay and, rank pay. In addition to this, you will receive a dearness allowance, as well as any category pension, in case you are found eligible.

For the purposes of commutation, only your basic pension is considered excluding DA or category pension.

How much can you commute and what are the specifics?

You can commute up to 50% of your basic pension. The period of commutation can be for 15 years. If the pensioner passes away during this period the family still gets to retain the commutation amount.

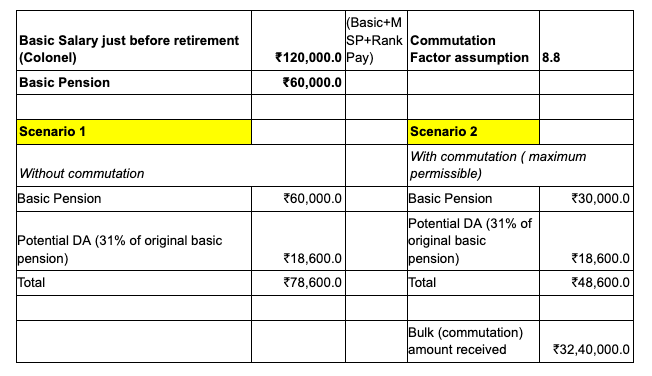

During this period you will receive a reduced pension. However, you will get an up-front lump sum which will be decided on a “factor of commutation”. This is dependent on the years of service as well as your age on retirement. Let’s see how it will look with an example.

What can we infer?

1. Commutation will give you a significant bulk amount (tax-free) but…

2. Your take-home pension will take a hit of up to 40%.

In what cases commutation may not be such a great idea?

Your monthly expenses are much more than your commuted pension and you don’t have any other source of income.

You expect much higher regular monthly expenses in the initial years of your retired life.

Investing your commutation lump sum – the main takeaways

Unless you plan to use the money for constructing your house or for some essential financial expense such as your child’s college tuition, you may consider investing the lump sum received as part of your commutation.

Here’s the first thing you need to keep in mind. What is your goal with this money in the future? Then consider the following:

If you will need all of this money in the next five years – consider fixed deposits or short term debt funds.

If you will need some (less than 50% of the money) in the next five years then consider investing what you will need in the short term in fixed deposits or short term debt funds.

If you don’t see yourself needing this money in the next 5 years or so consider investing at least 70% of this money in equity-based instruments such as in a good portfolio of equity mutual funds. The goal here is to stay ahead of inflation in the long term.

You can also invest the tax-free lump sum to generate an amount that can supplement your pension. Please talk to your financial planner to create a plan for this.

Comments

Post a Comment